Fear around money is the real deal and it can be downright paralyzing at times. You can’t seem to swim forward, and you realize that your ability to float just isn’t going to cut it after a while. Life raft needed! That was where I found Kristi when she reached out to me last July. She had her own money challenges and fears, and she was searching for a way to turn her situation into a money success story.

That was where I found Kristi when she reached out to me last July.

- Scared.

- Frustrated.

- Treading water.

Facing Fears

Before getting to that money success story, I asked her what she would feel like if her money challenges disappeared.

Her response, “I wouldn’t feel like a failure as a Mommy and as a person.”

Did your heart eyes just well up a bit? Mine too.

Damnit if money doesn’t have some kind of control over us if we let it. It had consumed Kristi to the point that she was doubting her abilities as a mother and an individual.

First things first? We had to take back control and not let any negative “money” stuff have any more of her mental effort than necessary. The plan?

- Reasonable, realistic budget aka liferaft

- Emergency fund, starter

- Debt payoff plan (prioritization) best plan of attack collection agencies/past due

- Progress towards debt (income/spending)

- Proactive planning – make sure to avoid the hole ever again

The area she guessed would be her biggest challenge? “I’m a tired Mom, feeding my kiddo.”

Can’t we all relate? Being exhausted physically and mentally can take us right through the drive-thru night after night and keep us from facing the pantry, tired and unmotivated for another pasta night.

Don’t worry, this is a money success story and has a happy ending, I promise – but we’re going to cover some dark topics with money management; fears, taxes, and collection companies…but all through the lens of a client SUCCESS story, scout’s honor.

Backwards Imaging

Kristi knew that change was on the horizon and it’s what she needed, but I had to make sure that she was ready for it by asking this question, ”What does life look like if you don’t change?”

Pausing from Kristi’s money success story for a minute and issuing you a challenge – if there is an area of your life that you are discontent with ask yourself this same question, “What does life like if I don’t change?”

Write down your response. Are you okay with staying where you are? Does your response light a fire under you to make a change?

Her response made it clear to me these thoughts were so close to the surface of her mind, that they were consuming much of her time and energy. Here’s what she said life would look like if something didn’t change.

- Kicked out of our apartment, and living with family

- Embarrassed by screwing it up as oldest sibling

- Bad example to son, not living his best family experience

- Not where I want to be

Fear is certainly not anything I’d wish on anyone, money related or otherwise – but it can serve as a motivator, and prompt positive change for some. These are some common financial fears.

Common Financial Fears

- Financial Instability: Many people fear not having enough money to cover their basic needs or unexpected expenses. The fear of losing a job or facing a financial crisis can be a very real concern. News cycles are full of layoff news on the regular.

- Debt and Financial Obligations: The fear of being overwhelmed by debt or being unable to meet financial obligations such as mortgage payments, credit card debt, or student loans is a common worry. This was a fear that Kristi was staring straight ahead at.

- Inadequate Retirement Savings: People often worry about not saving enough for retirement and being financially dependent on others or facing financial hardships during their later years. The number of “I wish we would have started earlier” comments from the 50-60 year olds I speak to is growing larger.

- Emergencies: Many individuals worry about unexpected emergencies such as medical expenses, home repairs, or car accidents, and the potential financial burden they may impose. Even a small starter emergency fund can help keep this fear at bay. Check out last months’ blog post about savings. Saving Money – How, What, Why and Where

- Lack of Financial Literacy: Some people fear not having the knowledge or skills to effectively manage their money, make sound financial decisions, and plan for the future. This also leads to a fear around how and what to teach our kids; this too was top of mind for Kristi with a young son.

- Inflation and Rising Costs: The fear of rising prices and the erosion of purchasing power can cause anxiety about being able to afford essential goods and services in the future. #eggs

Backstory

Kristi’s financial situation was not unlike others especially during the pandemic. She had moved across the country to be closer to family, incurring expenses greater than she anticipated, and found finding employment in 2020-2021 difficult to say the least. Y’all remember those COVID years, right?

Those shifts resulted in a few accounts going to collections, and loans from family keeping her afloat – and the progress she had found with her finances a few years back was now slipping through her fingers.

Kristi had every intention of paying what she owed and turning her situation around, and that meant facing a few tasks head on.

Living on less than you make is part of the equation when it comes to handling your finances well; so crafting a reasonable and sustainable budget was a staple – and working to get caught up and ahead of rent payments was our first order of business. That flip from behind 10 days, to being able to have rent ready and on time…doesn’t sound like much if you’ve never been there. But if you have, you know that swinging a 15-20 day shift on a $1700 rent payment is a big freaking deal. We celebrated!

Then we tackled another big item on list, Uncle Sam.

Filing Taxes

As we began working together, I found that Kristi was behind a few years on filing her taxes. A few years prior while working as a 911 dispatcher there had been a withholding snafu that left her with a hefty tax bill, along with a fear that the same could happen again.

Coming off of a few years of old loans going into collections, was a real fear of adding TO that problem when she filed her taxes. The typical action item of ‘file past tax returns’ was paralyzing for Kristi.

Now, taxes may not be your fear, but perhaps there is another daunting task that feels so big that you’d rather avoid it than tackle it.

Break it down into several mini steps instead.

- Gather up your tax documents. (She was 90% ready – but again, the fear around the act of actually filing kept her from finishing that last 10%.)

- Call a local tax prep service and make an appointment to drop off taxes.

- Go to the appointment when it comes time.

- Be available for any follow up calls as needed until taxes are completed.

Those four smaller bite size steps made the action item of ‘file past tax returns’ easier to tackle. And the results turned out as I had anticipated, with healthy refunds including past stimulus payments.

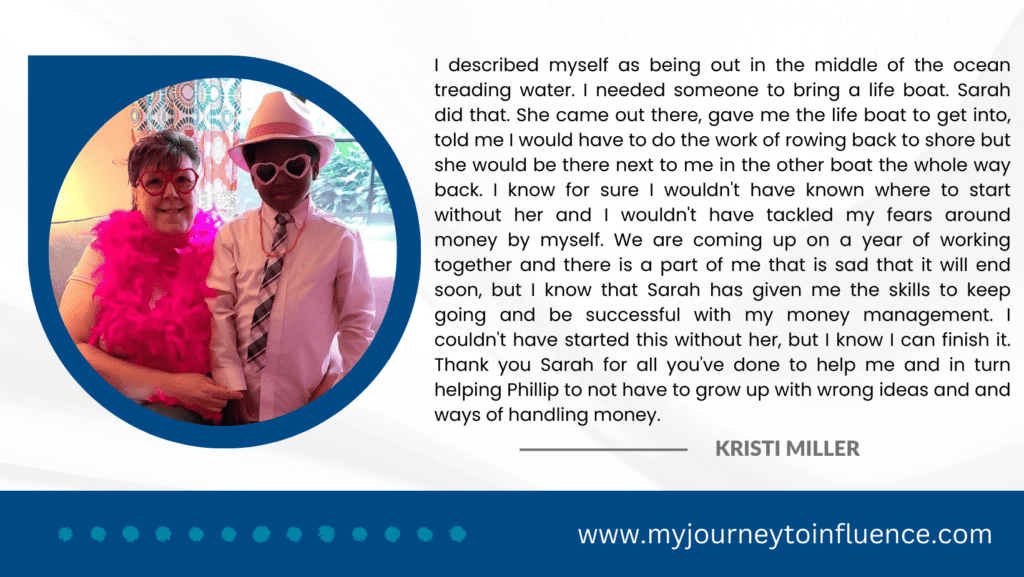

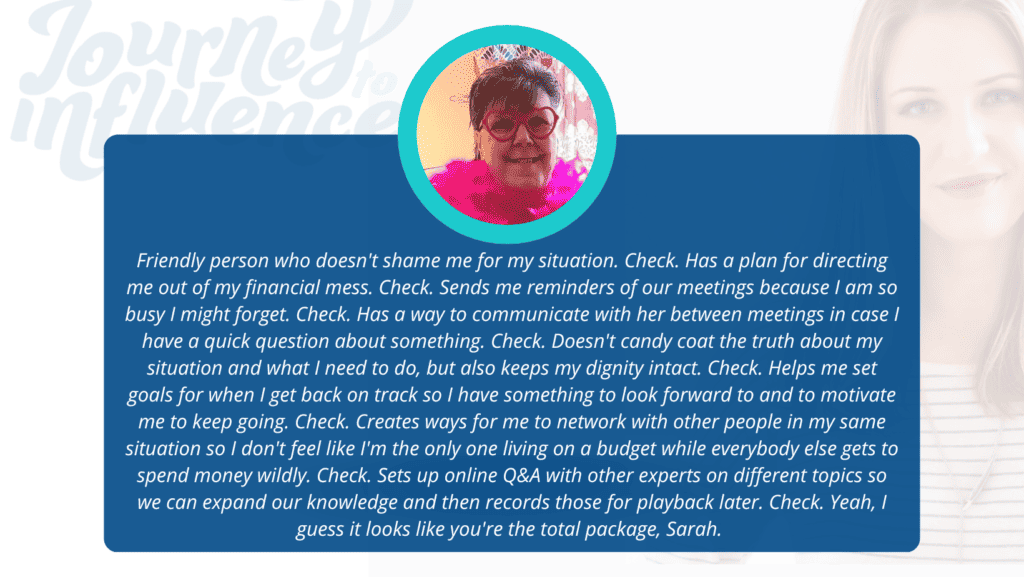

“I really appreciated being able to tackle the “scary stuff” slowly and in pieces. Having Sarah break things down into individual steps and accomplishments made it so much easier to take care of the intimidating tasks that needed to be handled.”

Kristi Miller

The celebrations we had as the tax preparer shared the news, the returns were filed, and those refunds came in helped to break down the fear that filing taxes had over Kristi – in fact her 2022 return was filed completely on time!

These refunds put her in a position to repay her family the money she had borrowed, and face her next challenge head on, the collection agencies.

Dealing with Collection Agencies

Kristi had a total of five items in collections that she was ready to tackle next, and we worked through this giant action item by again, breaking it down into smaller steps.

Dealing with collection agencies can be challenging, but there are a few best practices:

- Verify the Debt: Before engaging with a collection agency, verify that the debt they are claiming is legitimate. Request written validation of the debt, including details of the original creditor, the amount owed, and any relevant documentation. We called this simply fact finding, and gathering up the info.

- Understand Your Rights: Familiarize yourself with your rights as a consumer under the Fair Debt Collection Practices Act (FDCPA) or similar legislation in your country. This knowledge will help you understand what practices are prohibited and how you can protect yourself. Especially if you are getting hounded by creditors – know the limits here.

- Communicate in Writing: It’s generally recommended to communicate with collection agencies in writing rather than over the phone. Written communication provides a documented record of your interactions and allows you to maintain control of the conversation. Kristi made phone calls, she didn’t send out a carrier pigeon – but she did ask for settlement details in writing.

- Keep Calm and Be Professional: When communicating with collection agencies, maintain a calm and professional demeanor. Avoid getting emotional or hostile, as it may hinder productive discussions. Stick to the facts and focus on finding a resolution. Kristi found the representatives helpful, and she maintained a calm and kind disposition when dealing with them. (Did I mention that Kristi works as a dispatcher for an internet provider – she deals with customers and colleagues of all varieties on the phone daily, she’s a pro.)

- Negotiate a Settlement: If you’re unable to pay the full amount owed, try negotiating a settlement with the collection agency. Offer a lump sum payment or propose a payment plan that fits your financial situation. Be prepared to provide evidence of your financial hardship if applicable. Most debts are ‘sold’ from the original creditor to the collection company for pennies on the dollar – say 10% of what’s originally owed, so anything that they recoup above that is going to be a win for them…of course they’re going to aim for as close to 100% as possible. I believe that Kristi settled most of hers around the 50% mark. More great wins!!

- Keep Records: Keep copies of all written correspondence, payment receipts, and any relevant documentation throughout the process. This will serve as evidence in case of any disputes or inaccuracies in the future. AND you may need to reflect on this come tax time again, any resolution over $600 will likely result in a 1099-C a cancellation of debt that is included as income for your taxes – and one you’ll need to pay taxes on (or expect a reduction in your tax refund.)

- Consult with an Attorney or Credit Counseling Service: If you’re struggling to handle the situation on your own or facing complex legal issues, it may be helpful to consult with an attorney specializing in debt collection or a reputable credit counseling service. They can provide guidance based on your specific circumstances. Kristi handled her situation like a boss, and didn’t need added support – but in some situations this is certainly necessary.

Land Ahoy!

Kristi reaches shore in her life raft: taxes, plans, creditors, and an emergency fund in place for rainy Seattle days.

With her budgeting skills, she stays afloat, adapts, and ensures stability and resilience in any situation.

Kristi has proven to herself that she’s capable. As a great Mom, she tackles life one step at a time, overcoming setbacks with faith and inspiring tenacity.

As his Mom teaches and guides him, Philip will learn to live within his means, following their shared journey.

What’s Next?

Part 1: Sorting and Preparation

I’m so excited about what’s in store for Kristi and Phillip!

Preparing for a larger apartment, she sorts belongings into piles—keep, sell, toss—taking small steps towards her future move.

After Kristi’s hip replacement, she and Phillip will plan a trip to see the mouse in the near future. That’s right Disneyland is a bit rough without all the right joints! With newfound mental strength, Kristi can tackle challenges like hip replacement, purging, moving, and pursuing her dream job.

Part 2: A Journey of Resilience

Kristi, one of my biggest fans, sees me as her support on her life raft journey. Know that I’m also HER biggest fan. It’s not everyday that you meet someone that is willing to fight for what she believes in. Kristi dealt with adversity and challenges and refrained from ever being a victim. She was vulnerable, raw and full of faith. I’m so privileged to know her.

Friends with Budgets Community

This ‘network of people’ Q&A with experts, and quick question opportunity that Kristi speaks of comes in the form of the Friends with Budgets Community, a low cost membership to help…friends, with budgets – stick to those budgets with support and encouragement. Enrollment is now open!

Sign up below to get a weekly email with tips, tricks and truth about intentionality with your time, talent and money.